Ever stared at a mattress price tag and wondered if there’s a smarter way to pay? You’re not alone. Today we’ll break down the real financing options, from zero‑percent plans to credit‑friendly tricks, so you can snag the perfect smart bed without breaking the bank.

Smart mattresses can cost thousands of dollars. But you don’t need to pay it all at once. There are many ways to spread out the cost. Some are interest‑free. Others have low monthly payments. The trick is knowing which one fits your budget and your lifestyle.

Even though every smart‑mattress ad promises “0% APR,” the reality is a mixed bag of credit checks, hidden fees, and wildly different repayment terms. We looked at 11 different financing options from brands and third‑party providers. Here’s what we found: about a quarter of them require a hard credit check, and one option charges up to 36% APR. The same term length can mean either a cost‑free plan or a high‑interest loan. So you need to look past the headline rate.

Let’s walk through the nine best ways to finance a smart mattress in 2026.

1. SmartBeds.net’s Top Pick: Flexible Monthly Payments with 0% APR

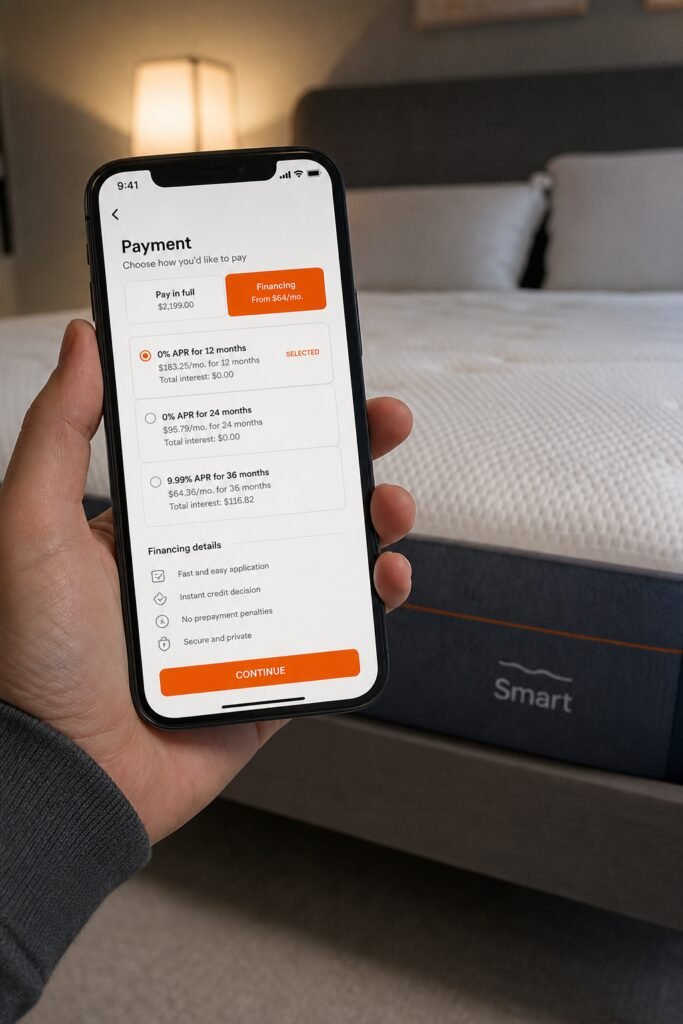

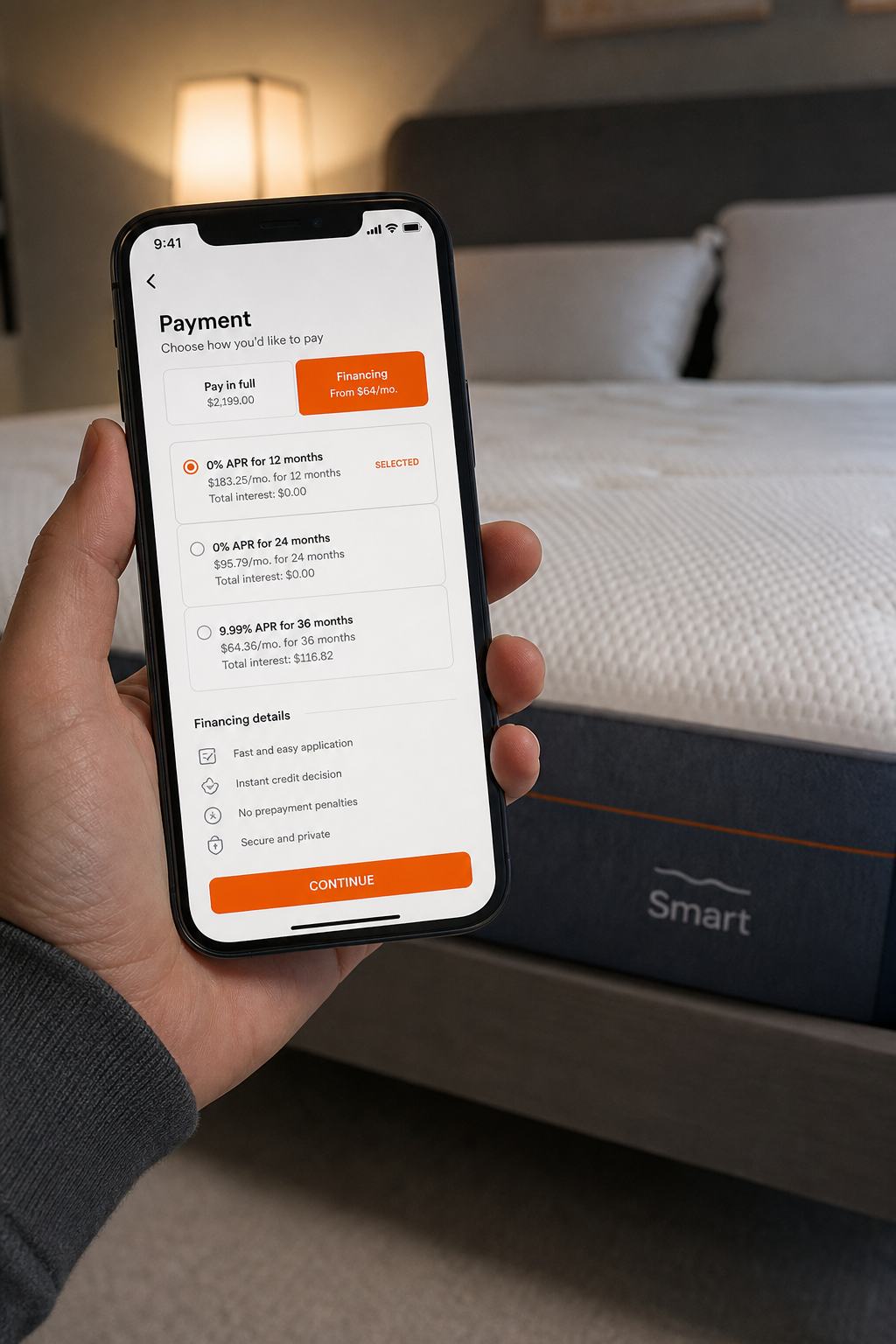

SmartBeds.net‘s recommended approach is using a flexible monthly payment plan. Many smart mattress brands offer this at checkout. You can choose to pay in full over 3, 6, 12, 18, or 24 months. Some plans come with 0% APR if you qualify. Other plans have rates from 10% to 36% APR, depending on your credit.

These services often perform a soft credit check when you check your options. That means it won’t hurt your credit score to see what you qualify for. If you accept a loan, the provider may report your payment history to credit bureaus. So making payments on time can actually help your credit.

One thing to watch: some plans require a down payment. And the total cost depends on the APR you get. For example, a $2,000 purchase at 15% APR over 12 months would cost about $181 per month. That’s still manageable, but you end up paying $172 in interest. Always check the exact numbers before you commit.

These plans are accepted at dozens of mattress retailers online. You can also use the provider’s app to manage your payments. There’s no penalty for paying early, so if you get a bonus or tax refund, you can save on interest.

According to the research we gathered, repayment terms can go up to 36 months, but the APR varies. It’s one of the few options that openly shows its rate range. That transparency helps you decide if it’s worth it.

If you want a flexible plan that works with many smart mattress brands, this is a solid choice. Just be sure you understand the APR before you click “buy.”

2. Buy Now, Pay Later Plans for Smart Beds

Another big name in the BNPL space offers four interest‑free payments every two weeks, or longer financing with rates. Many online mattress stores accept this method, including some that sell smart beds.

The “Pay in 4” plan is the simplest: you pay 25% today, then three more payments every two weeks. No interest, no fees if you pay on time. That works great for mattresses under $1,000. But for pricier smart beds over $2,000, you might need the longer installment option.

The longer financing can have interest rates from 0% to 29.99% APR, depending on your credit. They also do a soft pull for pre‑qualification, so it’s safe to check. Like other BNPL services, this provider will report your payments to credit bureaus.

One nice feature: some BNPL providers offer a card that lets you use their financing anywhere Visa is accepted, including mattress stores that don’t directly integrate that provider. That flexibility can be handy if you’re shopping for a smart bed at a local store.

Some users report that the provider’s app sends reminders and lets you postpone a payment once. That can be a lifesaver if you hit a rough month. Just be aware that late fees can apply, and they may affect your credit.

3. Deferred Interest Financing, No Interest if Paid in Full in 6 Months

Many deferred interest financing programs work a bit like a store credit card. You get a line of credit that you can use at any online merchant that offers such financing. For smart mattress purchases, they often offer promotional financing: no interest if you pay in full within 6 months. Some promotions go up to 24 months.

Here’s the catch: if you don’t pay off the entire balance by the end of the promotion, you’ll be charged interest from the purchase date at a high rate (usually around 26.99% APR). So you need to be disciplined. If you can pay off the mattress in six months, it’s essentially free money.

This type of financing is accepted at many smart bed retailers, including some smaller brands that might not offer other financing options. It’s also easy to link to an existing online payment account. You can manage payments through the provider’s app.

These programs typically do a hard credit pull when you apply. That can temporarily lower your credit score by a few points. But if you have good credit, you’ll likely qualify for the best promo offers. There’s no annual fee, and you can use the credit line for future purchases too.

For buyers who want a simple “interest‑free if paid on time” deal, deferred interest financing is a strong candidate. Just don’t forget the deadline.

4. Leading Smart Bed Financing, 24-Month 0% APR on Select Mattresses

One of the biggest names in smart beds offers financing through its own branded credit card, issued by a major financial partner. They often promote 24‑month 0% APR on select models. That means zero interest if you make the minimum monthly payments and pay off the balance within two years.

Their smart beds can cost $2,000 to $5,000. With 0% over 24 months, your monthly payment might be around $80 to $200. That’s pretty manageable for a high‑tech bed.

This financing requires a credit check. They’ll look at your credit score and history. Approval is more likely if you have good or excellent credit. If you don’t qualify for the 0% offer, they may offer a lower‑interest option instead.

One downside: the branded card can only be used at that brand’s stores and online. It’s not a general‑purpose credit card. So if you want to buy a different smart mattress brand, you’ll need another financing option.

But if you’re set on that brand’s bed, their own financing is hard to beat. The 0% APR for 24 months is one of the longest promotional terms available for smart mattresses. Plus, you get the brand’s smart tracking and adjustable firmness.

Our research shows that this is a classic “store card” model. It’s great if you love the brand. Just remember: if you don’t pay off the balance within 24 months, interest will be charged from the purchase date at a high rate.

5. Premium Smart Mattress Financing, 12-Month Special Financing with Equal Payments

Another premium smart mattress brand offers financing through their store credit card, issued by a well-known financing bank. They provide special financing: no interest if paid in full in 12 months. Minimum monthly payments are required.

These smart bases and mattresses can cost $3,000 and up. With 12‑month financing, you’ll need to pay roughly $250 to $400 per month to clear it in time. That’s a higher payment than longer terms, but you save on interest.

Like other store-specific cards, this one is restricted to that brand’s products. You can only use it for their items. But if you’re eyeing their premium smart base or adaptive mattress, it’s a convenient option.

Credit requirements are similar: you need good credit to get the 0% offer. If you qualify, it’s a solid deal. There’s also an option for longer terms with interest, but that’s less attractive.

A word of caution: the equal payments each month may not automatically pay off the balance by the end of the promo. You might need to pay a little extra to avoid the deferred interest. Always check your statement and make sure you’re on track.

6. Premium Store Card with Promotional Financing

Many high‑end department stores offer their own store card that provides promotional financing on furniture and mattress purchases, including some smart bed models. Often you’ll see “no interest if paid in full within 6 or 12 months” on qualifying purchases.

This type of store card can be used at the store’s own locations and sometimes at affiliated retailers. That’s helpful if you want to see a smart mattress in person before buying. Their selection includes leading smart bed brands and some adjustable bases with built‑in sleep technology.

The card may offer bonus rewards on purchases, which you can use toward future buys. But the main draw is the promotional financing. Just like other deferred‑interest offers, you must pay the full balance before the promo ends to avoid retroactive interest.

Credit check is a hard pull. Approval odds are better if you have a good credit score (680+). The ongoing APR after the promo is high, around 27% to 30%, so it’s wise to pay off the balance before the promotional period ends.

7. Credit Card with 0% Intro APR for Large Purchases

A general‑purpose credit card with a long 0% intro APR period on purchases offers a flexible way to finance a smart mattress. As of early 2026, some cards offer 0% for 21 months on new accounts. That gives you almost two years to pay off a smart mattress with zero interest.

This is a great option for people who want to avoid store‑specific cards. You can use a card like this for any purchase, including from your favorite online mattress seller. There’s no annual fee and no penalty for late payments (though late fees still apply).

To get this card, you’ll need good to excellent credit. The 0% APR applies only to new accounts, and it’s fixed for the promotional period. After that, the variable APR is around 19% to 29%.

One downside: you won’t earn rewards. But if your goal is interest‑free financing, the rewards trade‑off is worth it. You could also pair it with a cashback card for the initial payment, but that’s more complicated.

Using a 0% APR card requires discipline: you must make at least the minimum payment each month and pay off the full balance before the intro period ends. Otherwise, the remaining balance will be subject to the standard APR.

If you qualify, this type of card gives you flexibility to shop any brand. Combined with a smart mattress that fits your needs, it’s a powerful combo.

8. Lease-to-Own with No Credit Needed

Some lease‑to‑own providers offer financing on furniture, including smart mattresses. You pay weekly or monthly payments for a set term (usually 12 to 24 months), and at the end you own the bed. No credit check is required. They approve based on income and identity verification.

This is a good option if you have poor or no credit. The downside: the total cost is often much higher than the retail price. You might end up paying double or more over the lease term. For example, a $2,000 smart bed could cost $4,000 with weekly payments of $35 for 24 months.

Some lease‑to‑own companies offer a “same as cash” option where you pay off the bed early and avoid extra fees. If you have the discipline to pay it off within 90 days, you can save a lot. But if you stretch payments out, the cost adds up.

Another catch: late payments can result in additional fees, and missing payments can lead to the bed being repossessed. It’s risky, but it can work if you need a smart mattress now and have no other financing options.

9. Personal Loans with Fixed Rates for Smart Mattress Purchase

Online personal lenders offer loans up to $100,000 with fixed rates from about 8% to 25% APR. You can use the loan for any purpose, including buying a smart mattress. Terms range from 24 to 84 months. With good credit, you may get a rate lower than most credit cards.

Personal loans have a fixed monthly payment, which makes budgeting easy. There are no prepayment penalties, so you can pay it off early and save on interest. Some lenders also offer unemployment protection: if you lose your job, they may pause your payments and help you find work.

To get a loan from these lenders, you’ll need good credit (690+). They do a soft pull for pre‑qualification, then a hard pull when you accept. The loan is funded quickly, often within a few days.

The main advantage is that you can shop for any brand without being locked into a store card. The disadvantage is that even with a low rate, you’ll pay interest over the term. For a $3,000 mattress at 10% APR over 36 months, you’d pay about $97 per month and $480 in interest.

Personal loans are best for those who want predictable payments and don’t qualify for 0% offers. They’re also good for bundling a mattress with other purchases.

How to Choose the Right Financing Option for Your Smart Mattress

With so many choices, how do you pick? Start with your credit score. If you have good or excellent credit (680+), you can aim for 0% APR offers from store cards or third‑party providers like online installment lenders and buy now, pay later services. If your credit is fair or poor, look at no‑credit leasing options or a personal loan from a lender that works with lower scores.

Next, decide how quickly you can pay off the mattress. If you can pay within 6 months, use a short‑term online credit account or a store card with a 6‑month promo. If you need more time, a long‑term 0% APR credit card with a 21‑month intro period is ideal. For longer terms, the mattress brand’s own 24‑month 0% APR program or a personal loan with a low rate may work.

Consider the total cost. A 36‑month plan at 0% is free money. But a 36‑month plan at 20% APR adds a lot of interest. Always calculate the total payment amount, not just the monthly payment.

Watch for fees. Most plans have no fees, but some leasing options have high effective interest. Also understand what happens if you’re late. Deferred interest plans can charge back interest from day one if you miss the deadline.

Finally, check if the mattress brand has special financing partnerships. Some smaller brands work with third‑party lenders to offer 0% APR. It’s always worth clicking “check financing” at checkout to see your options , it’s usually a soft pull.

If you’re still overwhelmed, our guide on how smart beds work can help you understand what features matter, so you don’t overpay for tech you won’t use.

Frequently Asked Questions

What credit score do I need for smart mattress financing?

It depends on the option. Store cards from some mattress brands and general credit cards typically require a score of 680 or higher for 0% APR offers. Some third-party financing providers are more flexible, accepting scores in the mid‑600s for their best rates. Some rent-to-own services don’t check credit at all. Always check the specific requirements before applying.

Can I finance a smart mattress with bad credit?

Yes, but your options are limited. Some rent-to-own services accept almost anyone with a valid ID and income. Some third-party financing providers may still approve you, but you’ll get a higher APR. Some brands also offer lease‑to‑own through certain providers, which doesn’t require good credit. Expect higher costs, so try to pay off the mattress as quickly as possible.

Does financing a smart mattress hurt my credit?

Applying for most store cards or general credit cards results in a hard inquiry, which can lower your score by a few points temporarily. Some thin‑file loans do a soft pull upfront, but if you accept the loan, your payment history may be reported. Making on‑time payments can help your score. Missing payments will hurt it.

What happens if I miss a payment on 0% financing?

For deferred‑interest plans, missing the final payment deadline triggers interest from the purchase date at the regular APR, which can be 25% or higher. For some installment plans, you’ll be charged late fees and interest may accrue. Always set reminders or automatic payments to avoid costly mistakes.

Can I return a smart mattress if I financed it?

Yes, most brands allow returns during the trial period even if you financed. For example, many brands’ trial periods apply whether you pay cash or use financing. If you return the mattress, the financing will be canceled, and you’ll get a refund for payments made minus any interest already charged. Check the return policy before buying to avoid surprises.

Is it better to finance through the mattress brand or use a general credit card?

If you plan to buy from a specific mattress brand, their store‑specific financing often offers longer 0% terms. A general 0% intro APR card gives you more flexibility across brands. Choose the option that aligns with your credit score, the mattress you want, and how quickly you can pay it off.

How long do I have to pay off a financed smart mattress?

Promotional terms range from 6 to 60 months. Six‑month plans are common with some deferred-interest options and store cards. Twelve to 24 months is typical for 0% offers from some mattress brands. Personal loans can stretch 36 to 84 months, but you’ll pay interest. Pick a term that fits your budget but doesn’t drag out the cost.

Are there any hidden fees in mattress financing?

Most 0% APR plans have no fees if you pay on time. Watch out for deferred interest , if you miss the payoff deadline, you’ll be charged back interest. Some lease‑to‑own options have application fees or late fees. Always read the fine print before signing. For example, some furniture store credit cards have a $2 minimum interest charge. Stay informed.

Conclusion

Smart mattress financing doesn’t have to be confusing. The key is to match the option to your credit profile and how fast you can pay. If you have excellent credit, go for 0% APR offers like 24‑month plans from premium brands or long intro period cards. If your credit needs work, consider lease‑to‑own or a personal loan from reputable online lenders.

Remember the research we started with: not all 0% offers are equal. Some come with credit checks, and the same term length can be either a great deal or a trap. Always calculate the total cost, not just the monthly payment. And set reminders to pay off promotional balances before they expire.

At SmartBeds.net, we want you to sleep well and rest easy. That includes peace of mind about your purchase. Check out our top smart mattress picks for 2026, and combine them with the best financing option for your situation. You deserve a mattress that helps you thrive, and now you have the tools to afford it without stress.

If you’re still unsure which route to take, start with a soft‑check tool like pre‑approval offers from various lenders. It won’t hurt your credit, and you’ll see your real options in minutes. Then pick a mattress you love and a plan that fits your life. Sleep well, friends.